Wondering whether a character-filled loft or an amenity-rich high-rise will deliver better returns in River North? You want reliable cash flow, manageable risk, and strong resale value in a neighborhood that moves fast. This guide gives you the local context you need and a simple model to compare net yields, assess risk, and plan for capital projects. Let’s dive in.

Loft vs high-rise: what you’re buying

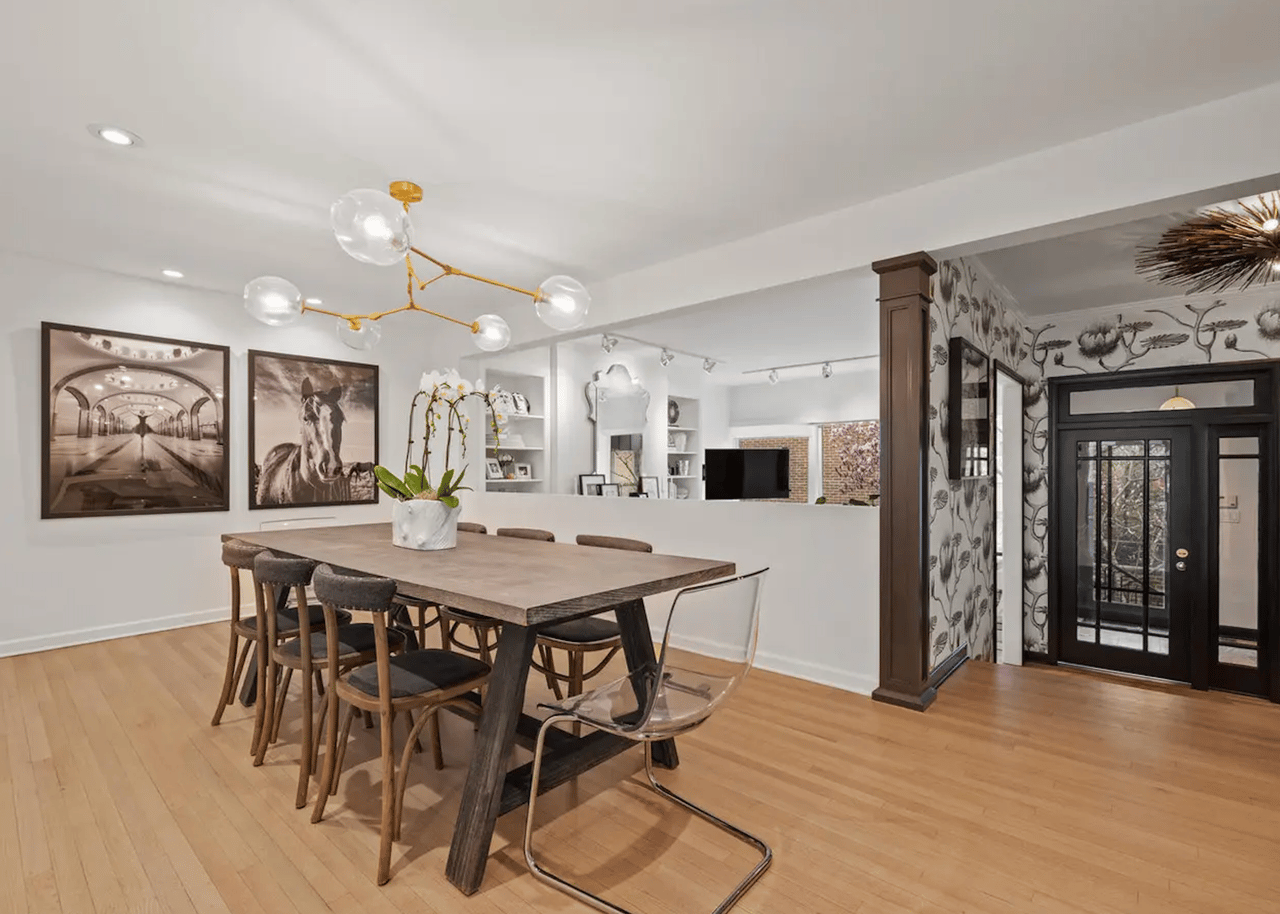

Lofts in River North are typically early 20th-century warehouse conversions. You’ll see open layouts, tall ceilings, and exposed brick or timber, with fewer on-site amenities. Associations are often smaller, which can mean lower monthly dues but more variability in reserves and special assessments.

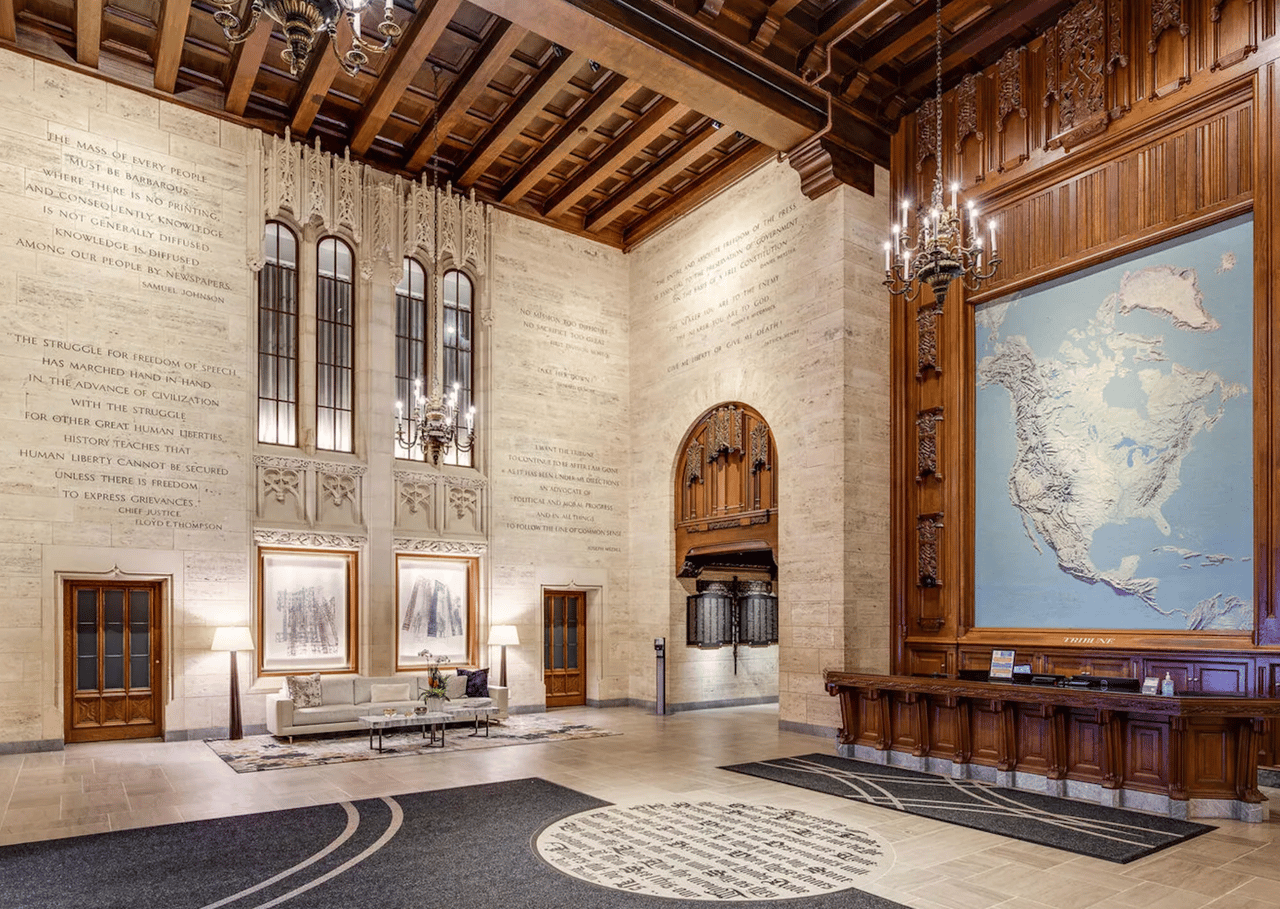

Modern high-rises offer smaller footprints and extensive amenities like doorman service, fitness centers, package rooms, and sometimes pools or parking. Professional management and larger associations can support stronger reserves, but monthly assessments are typically higher.

Both product types rent well, but to different audiences. Lofts attract design-minded renters and households that want space and character. High-rises appeal to professionals and corporate renters who value services and security.

How returns differ in River North

Return drivers split into two core tradeoffs:

- Rent premium vs operating cost. High-rises can command higher per-square-foot rents, but the higher HOA cuts into net yield. Lofts may carry lower HOA and solid per-unit rents, but capital maintenance can be lumpier.

- Liquidity vs niche value. High-rise units with amenities are broadly marketable on resale. Unique loft layouts can achieve premiums with the right buyer, though the pool may be smaller.

To compare apples to apples, you need to account for rent, HOA, taxes, insurance, utilities, management, vacancy, and capital reserves. In Chicago condos, HOA inclusions matter. If heat, water, or other utilities are included, your rent may be higher, but so is your fixed monthly cost.

Revenue realities and leasing dynamics

Who rents your unit shapes rent, vacancy, and turnover:

- High-rise tenants: professionals and corporate renters who value security and services. They accept efficient footprints and may consider furnished or semi-furnished leases, subject to building rules.

- Loft tenants: creative professionals and design-focused renters who want larger single-floor plans and character. They often seek 1 to 2 bedrooms with flexible layouts.

Most investor leases run 12 months. Corporate or furnished terms can range from 3 to 12 months, but confirm association rules. City of Chicago short-term rental licensing and many condo bylaws restrict non-owner-occupied short stays. Plan for standard annual leases unless you confirm both city licensing and building approval.

The simple model: compare net yield

Collect these inputs for each candidate condo:

- Purchase price (P)

- Expected monthly rent (R_month)

- Monthly HOA/assessment (HOA)

- Monthly property taxes (T_month)

- Monthly insurance (I_month)

- Owner-paid utilities (U_month)

- Property management fee as a percent of rent (Mgmt%)

- Vacancy allowance (Vacancy%)

- Annual capital reserve as a percent of price (CapEx%)

- Optional: mortgage payment for cash-on-cash analysis

Key calculations:

- Annual gross rent = R_month × 12

- Vacancy allowance = Annual gross rent × Vacancy%

- Effective gross income (EGI) = Annual gross rent − Vacancy allowance

- Operating expenses (annual) = (HOA × 12) + (T_month × 12) + (I_month × 12) + (U_month × 12) + (Mgmt% × Annual gross rent) + routine maintenance allowance

- Annual CapEx reserve = P × CapEx%

- Net operating income (NOI) = EGI − Operating expenses − CapEx reserve

- Net yield (NOI yield) = NOI ÷ P

Guidelines to set assumptions:

- Vacancy: 5 to 10% for stable 12-month rentals; higher if furnished or shorter terms.

- Management: 6 to 10% of rent for full-service management.

- CapEx reserve: 0.5 to 1.5% of purchase price per year; lean higher for older lofts and lower for newer high-rises.

Illustrative examples only. Replace with actual comps before deciding:

- Loft scenario (hypothetical): P = $550,000 | R_month = $3,200 | HOA = $400 | Taxes = $600 | Insurance = $60 | Utilities owner pays = $0 | Mgmt% = 8% | Vacancy% = 7% | CapEx% = 1.25%.

- High-rise scenario (hypothetical): P = $650,000 | R_month = $3,800 | HOA = $1,100 (includes some utilities) | Taxes = $700 | Insurance = $60 | Mgmt% = 8% | Vacancy% = 6% | CapEx% = 0.75%.

Run the formulas to calculate NOI and NOI yield for each. Then compare which inputs drive the gap in returns.

Sensitivity: test your downside

Stress-test your assumptions to see how resilient each option is:

- Increase vacancy by 2 to 5 percentage points and note the NOI change.

- Raise HOA by 10 to 20% to simulate fee increases or new staffing costs.

- Add a one-time special assessment and either apply it in year 1 or amortize it over 3 to 5 years.

- Lift CapEx% for older loft buildings and re-run the model.

This exercise highlights sensitivity to HOA and vacancy. It also clarifies the break-even rent you need to cover HOA, taxes, and reserves.

Due diligence: documents and questions

Before you write an offer, request these items:

- Condo declaration, bylaws, rules, and rental policies

- Two to three years of budgets and audited financials

- Current reserve study and reserve fund balance

- HOA meeting minutes for the last 12 to 24 months

- List and status of any special assessments

- Master insurance certificate and coverage summary

- Claims history for major incidents

- Rental mix, if available, to understand investor vs owner-occupant ratios

- Parking deed or lease details, if applicable

Targeted questions to ask:

- Are rentals limited by a cap or registration process? Minimum lease term?

- Are short-term or corporate rentals allowed, and under what conditions?

- Which capital projects are planned in the next 5 years, and how will they be funded?

- How often do HOA dues increase, and by how much historically?

- What is the history of special assessments over the last 10 years?

Capital cycles and value retention

High-rises face predictable big-ticket items like façade work, elevators, risers, boilers, garage repairs, and amenity refreshes. Well-funded reserves and proactive projects support resale value and buyer confidence.

Lofts often require window replacement, roof work, moisture remediation, and electrical or plumbing upgrades. Interior improvements inside the unit can be more common if you want to compete with newer finishes.

In both cases, finishes and layout relevance matter. Homes that show well lease faster and hold value better. The association’s ability to plan and fund capital work is a key driver of long-term price stability.

Which fits your goals?

Choose based on your priorities and time horizon:

- Prioritize stable liquidity and broader renter appeal. A high-rise with strong amenities and professional management often attracts a wide tenant pool and may support liquidity in varied markets, albeit with higher monthly HOA.

- Seek lower fixed costs and character-driven demand. A loft can produce attractive NOI if the HOA is efficient and the association manages capital projects well. Budget more for reserves and be prepared for a more niche renter and buyer pool.

- Considering furnished or corporate leasing. Verify building rules and city licensing early. Many associations restrict short-term rentals or impose minimum lease terms.

Next steps

- Identify specific loft and high-rise comps in River North and collect actual rents and HOA figures.

- Obtain condo documents, recent budgets, and a reserve study before commitment.

- Run the net yield model with your verified inputs, then stress-test for vacancy, HOA changes, and assessments.

- Confirm rental policy, short-term rules, and any city licensing requirements.

- If you want building-level insight, rent comps, and a clean underwriting model tailored to your goals, connect for a private discussion.

For discreet guidance and a building-by-building comparison tailored to your strategy, schedule a conversation with Mike Larson.

FAQs

What is the difference between a River North loft and a high-rise condo?

- Lofts are converted warehouse buildings with open layouts and fewer amenities; high-rises are modern towers with services like doorman and fitness centers, which often means higher HOA.

How do HOA dues in Chicago condos impact net yield?

- HOA is a fixed monthly cost that directly lowers NOI; higher HOA can offset higher rent, so always model HOA inclusions, expected increases, and reserves alongside rent.

Are short-term rentals allowed in River North condos for investors?

- Many buildings restrict short-term rentals, and the City of Chicago requires licensing; assume 12-month leases unless you confirm both building approval and city compliance.

What vacancy rate should I use for a River North investment condo?

- A common range is 5 to 10% for standard 12-month leases, with higher allowances for furnished or shorter-term arrangements.

How should I plan for special assessments and capital projects?

- Review reserve studies, budgets, and meeting minutes, then model a contingency for assessments and maintain an annual CapEx reserve of roughly 0.5 to 1.5% of price.

Which has better resale liquidity in downtown Chicago: loft or high-rise?

- High-rise units with amenities typically appeal to a broader buyer pool; unique lofts can achieve premiums with the right buyer but may be more niche during slow markets.